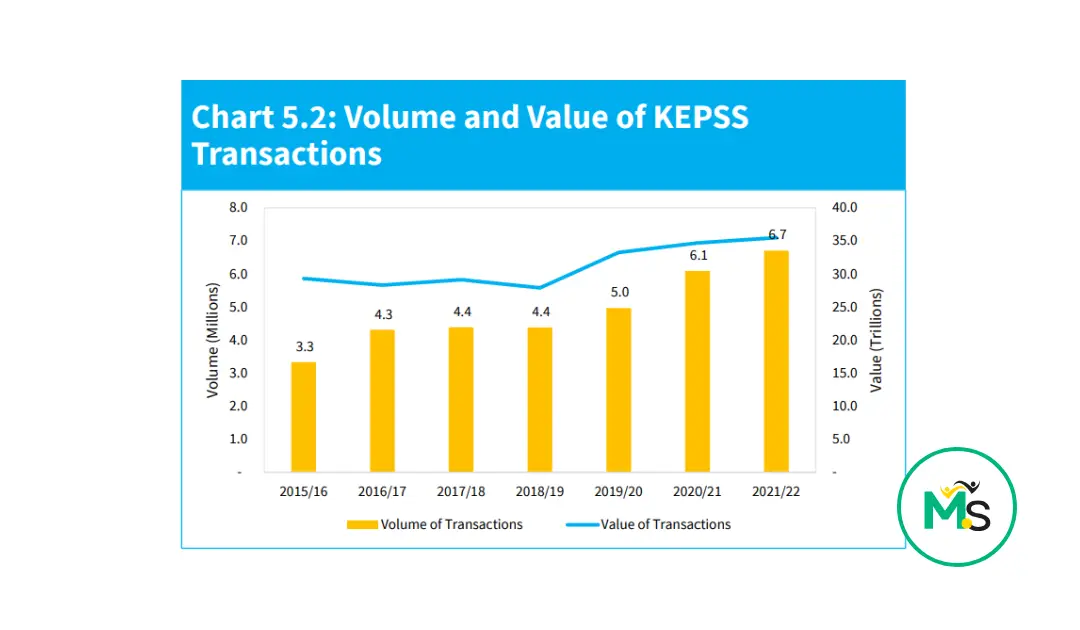

The Kenya Electronic Payment and Settlement System (KEPSS) is a Real Time Gross Settlement (RTGS) system, meaning that transactions are cleared and settled continuously and in real time.

It is Kenya’s only systemically significant payment system used for large value and time-critical payment instructions.

KEPSS was implemented in 2005 and is operated by the Central Bank of Kenya.

The rules and procedures for KEPSS apply to all participants for their transactions in the system.

1")

KEPSS operating hours

| Time schedule | Activities and Available Transactions |

|---|---|

| 8:30 am Start-of-Day | KEPSS start-of-day |

| 8:45 am – 2:00 pm Operating Day Commences | Window 1 – Participants can send and receive payments. – The Bank enters Net Settlement Instructions from approved Clearing Houses. – Account transfers and its own payments. |

| 2:00 pm – 4:00 pm Initial Cut-off | Window 2 – Closed to new payments, except for bank-to-bank (MT2XX series) and Account Transfers. – Queue clearance may be effected by application of gridlock resolution tools by the Bank and by deletion of queued payments by Participants. – Participants must arrange to have sufficient available funds to allow the reversal of ILF drawings prior to the Final Cut-off. |

| 4:00 pm Final Cut-Off | – No further inputs accepted. – After the final cut-off queue/settlement processing will cease and any transactions still in queues will be rejected with MT097 issued to SWIFT and passed by SWIFT to the relevant Participant. |

| 4:30 pm System Close | – End-of-day processes, such as reports, archiving. |

Participants’ connection requirement:

Participants are required to be connected to the KEPSS system to facilitate the execution of transactions according to the specified operating schedule.

In summary, KEPSS plays a critical role in Kenya’s financial infrastructure by facilitating efficient, secure, and real-time settlement of large-value and time-sensitive payments between banks and other financial institutions.